News about HMRC and savings always spreads fast, but stories involving ISAs travel even quicker because they hit a nerve for millions of UK savers. Individual Savings Accounts are seen as one of the safest and most straightforward ways to grow money tax‑free, so when people hear about an “HMRC crackdown” and thousands of letters being issued, the first reaction is usually worry.

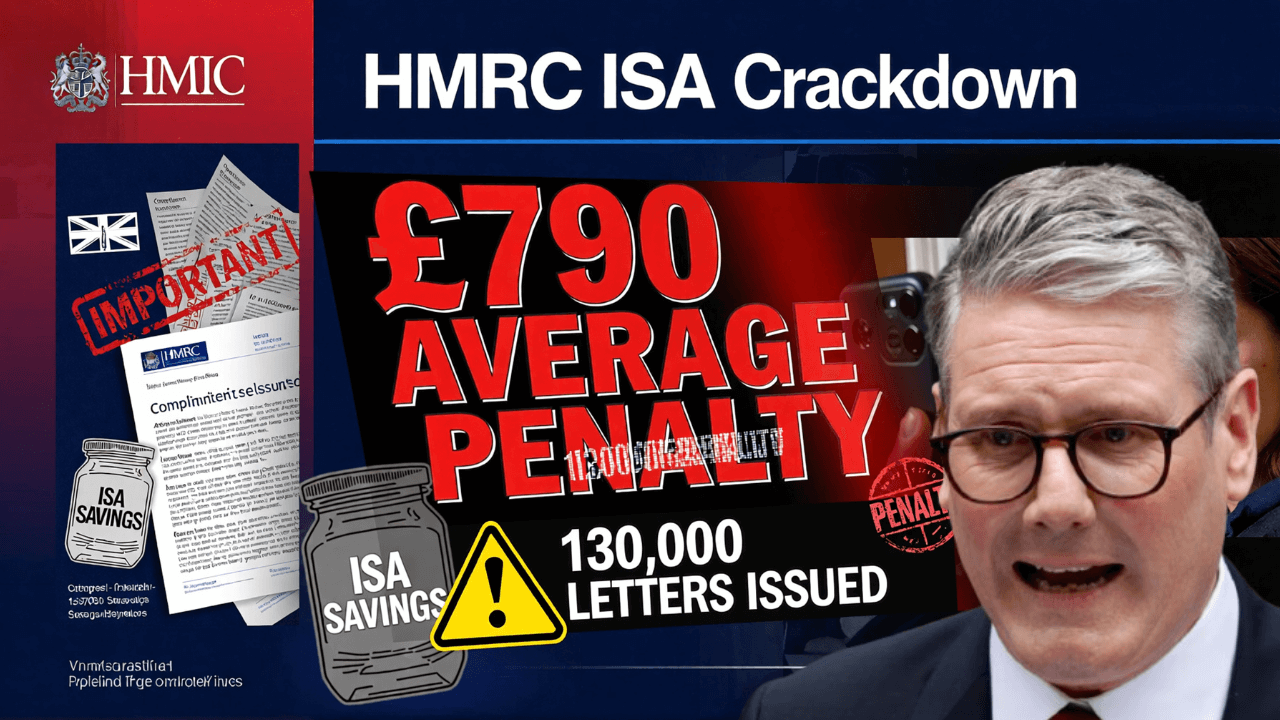

The headline claiming 130,000 letters have been sent with a £790 average penalty has sparked a lot of questions. Are ISA savers being punished? Has HMRC changed the rules? Can you be fined even if you did not do anything wrong? And what should you do if a letter arrives in the post?

The most important thing to understand is that an HMRC letter does not automatically mean you are in trouble. Often it is a warning, a request to correct something, or a notice triggered by data mismatches. Still, it is not something to ignore, because ISA rules are strict and mistakes can sometimes lead to penalties, tax charges, or forced corrections that reduce the tax‑free benefit of the account.

This article explains what this “crackdown” really means, why HMRC sends letters to ISA savers, how a penalty like £790 can happen, and what UK residents can do now to stay on the safe side.

Why ISA letters from HMRC are creating panic

ISAs are popular because they are designed to be simple. Many savers treat them as a “set and forget” product. You open one, deposit money regularly, and assume everything is protected from tax forever.

So when people hear about a large volume of letters being issued, it sounds like a sudden policy change or a new penalty system. It also feels personal. Savers may worry that HMRC is monitoring their accounts or that they might be forced to pay money back.

In reality, HMRC has always monitored ISA subscriptions using data reported by ISA providers. The difference is that more checks, better automation, and stronger data matching can make enforcement feel more visible than before.

What HMRC means by an ISA “crackdown”

The word “crackdown” is often used in headlines because it sounds serious. But in practice, it usually means HMRC is actively identifying cases where ISA rules may have been broken and contacting savers to correct those cases.

HMRC is not trying to discourage people from using ISAs. ISAs are a government‑approved, tax‑efficient savings product. The purpose of enforcement is to make sure the tax‑free benefit is only applied within the rules.

Most crackdowns focus on situations such as over‑subscriptions, incorrect account types, or duplicate subscriptions that break the annual allowance rules.

What the 130,000 letters likely represent

A figure like 130,000 letters suggests HMRC has flagged a large number of ISA accounts for review or correction. This does not mean 130,000 savers have been fined, but it does suggest HMRC believes those cases may involve errors or inconsistencies.

Some of these letters may be informational or corrective rather than punitive. Many are likely sent because the system detected something that looks wrong and HMRC wants to clarify what happened.

It is also worth remembering that one saver can sometimes receive more than one communication if an issue spans multiple tax years or involves multiple providers.

Why the £790 “average penalty” figure is confusing

The phrase “average penalty” can easily be misunderstood. It makes people imagine that every saver receiving a letter will be charged £790. That is not how HMRC normally operates.

An average could include a mix of small penalties and a smaller number of much larger penalties, which pushes the average up. It could also include interest or tax adjustments included in the total.

The key point is that £790 is not automatically what you will pay just because you have an ISA. Any penalty depends on the nature of the issue and how it is corrected.

The most common reason: exceeding the ISA allowance

One of the biggest reasons people get into trouble with ISAs is exceeding the annual ISA allowance. The allowance is a total cap across all ISA types combined within the tax year.

Many savers forget that the ISA limit is not per account, and not per provider. It is one combined total.

People can exceed it accidentally if they have several savings products, move money around during the year, or contribute through different apps and banks without keeping track of the total.

The “two providers” mistake that traps savers

Another common issue is opening a second ISA of the same type in the same tax year and paying into both. Rules around subscribing to ISAs can be confusing, especially when banks advertise new “best rate” deals and encourage switching.

A saver may open a new Cash ISA at a different bank for a better rate and continue paying into the old one by accident. That creates a rule breach even if the saver stays under the total allowance.

This is the type of mistake HMRC systems can detect once providers submit annual ISA reports.

Why switching ISAs can create problems

Switching ISAs is allowed, but it has to be done correctly. If you withdraw money and redeposit it into a different ISA, that can count as a fresh contribution depending on how it is done.

Many people assume that moving money between ISAs is always neutral, but HMRC rules depend on whether you used a formal ISA transfer process or you took the money out yourself.

Mistakes here can lead to over‑subscriptions without the saver realising, especially if the money moved is large.

When withdrawals and re‑deposits become risky

Some ISA providers offer flexible ISA features where withdrawals can be replaced without using more allowance. But this depends on the ISA being flexible and on the money being replaced within the correct timeframe and rules.

If someone withdraws from an ISA, spends it, then later repays it, they may assume it is simply “putting the money back.” But depending on the ISA type, that repayment may count as a new subscription.

This is why savers who frequently move money in and out are sometimes more exposed to accidental breaches.

Why HMRC’s data matching is getting stronger

Most ISA issues are discovered through provider reporting. ISA managers send information to HMRC about subscriptions, account types, and totals. HMRC then checks whether contributions align with the rules.

As digital banking becomes more common, reporting becomes faster, more accurate, and easier to analyse. That means HMRC can flag issues more reliably, and letters may be issued more frequently than people are used to.

For savers, this is not necessarily a threat. It is simply a reminder that errors are easier to spot now than they were years ago.

Who is most at risk of receiving an HMRC ISA letter

Not every ISA saver is equally likely to get a letter. The people most at risk are typically those who use multiple accounts across different providers, switch regularly for better rates, or contribute in larger lumps rather than small monthly deposits.

Higher‑balance savers may also be more visible in reporting, simply because their annual movements and contributions are larger. People who manage finances for someone else, such as an elderly parent, can also be exposed to mistakes if the person has more than one ISA and the family is unaware.

Even then, most cases are errors rather than fraud.

What an HMRC letter may ask you to do

If HMRC contacts you, the letter may ask you to confirm details, review subscriptions, or explain why a contribution breach happened. In some cases, it will outline steps HMRC intends to take to correct the situation.

Sometimes the letter will explain that an ISA has been declared invalid for a portion, meaning the tax‑free status may not apply to certain funds. In other cases, the letter could instruct you to contact your ISA provider, or it could explain that HMRC is adjusting the situation automatically.

The exact wording matters, which is why reading the full letter carefully is essential.

Does an HMRC ISA letter mean your money is in danger

For most savers, no. HMRC letters do not mean your savings are being seized. They are about correcting tax treatment, not removing access to your funds.

However, it can affect the tax‑free benefit if you have broken the rules. That could mean paying tax on interest or gains that would otherwise have been tax‑free, or in some situations facing penalties or corrections that reduce the benefit of the account.

So while the money is still yours, the tax advantages may change if the ISA was not handled correctly.

Why penalties can happen even when mistakes are accidental

Many people assume penalties only happen if you deliberately break rules. But tax systems often apply penalties based on outcomes, even when the mistake was accidental.

The difference is that accidental mistakes may be treated more lightly if you respond quickly and cooperate. HMRC often looks at whether the saver made a genuine error or ignored warnings and continued breaching rules year after year.

This is why acting promptly after receiving a letter is one of the best ways to reduce stress and potentially limit consequences.

What you should do if you receive an HMRC ISA letter

The first step is to stay calm. ISA letters can look intimidating, but many issues can be resolved.

The second step is to verify the letter is genuine. HMRC scams do exist, and criminals often use fear and urgency. A real HMRC letter will not demand immediate payment through unusual methods or ask for bank passwords.

Once you are confident it is real, check your own records. Look at how much you subscribed during the tax year, which ISAs you paid into, and whether you used formal transfer routes when switching providers.

If needed, contact your ISA provider for contribution summaries. Most providers can confirm how much was subscribed in that tax year.

What not to do after getting the letter

The worst option is ignoring it. Even if you believe it is wrong, you should still take action to clarify the situation. Ignoring official communication can lead to follow‑ups that feel more severe later on.

It is also risky to panic‑withdraw money immediately. Sudden withdrawals can create further confusion and may not fix the issue, especially if the breach is already recorded.

The best approach is simple: understand the claim, confirm your numbers, and respond as instructed.

How to avoid ISA mistakes in 2026 and beyond

The safest way to avoid ISA trouble is to track subscriptions during the year, especially if you have more than one account. It helps to keep notes of where you are paying in and how much is going into each product.

If you want to switch ISAs, use the official ISA transfer process offered by providers rather than withdrawing the money yourself. That protects the tax‑free status and reduces the chance of accidental rule breaches.

If you use flexible ISAs, read the provider’s rules carefully so you understand how withdrawals and replacements are handled.

Why ISA savers should not stop using ISAs because of headlines

It can be tempting to think ISAs are “too risky” after seeing stories like this. But ISAs remain one of the most effective and widely used tax‑free savings tools in the UK.

The issue is not that ISAs are unsafe. The issue is that the rules are strict, and mistakes can happen when savers use multiple providers without tracking contributions.

For most people, staying organised is enough to avoid problems, and the benefits of tax‑free savings remain strong.

Final thoughts

A headline about 130,000 letters and a £790 average penalty sounds frightening, but it does not automatically mean millions of ISA savers are about to be fined. In most cases, HMRC letters are triggered by rule breaches such as over‑subscription, paying into multiple ISAs incorrectly, or switching mistakes that confuse the allowance rules.

The smartest thing any saver can do is treat the letter seriously, check the details, and respond calmly. If you are proactive, most ISA issues can be corrected without long‑term damage.

ISAs are still an excellent way to save and invest tax‑free in the UK. The key is using them confidently and correctly, rather than relying on guesswork or assuming providers automatically prevent every mistake.